The CRTC has released their annual “Communications Monitoring Report” and there’s a bunch of notable stats. Jean-Pierre Blais, Chairman of the CRTC, stated “this report is used to gauge whether the communications industry is meeting the needs of Canadians as consumers, citizens and creators.”

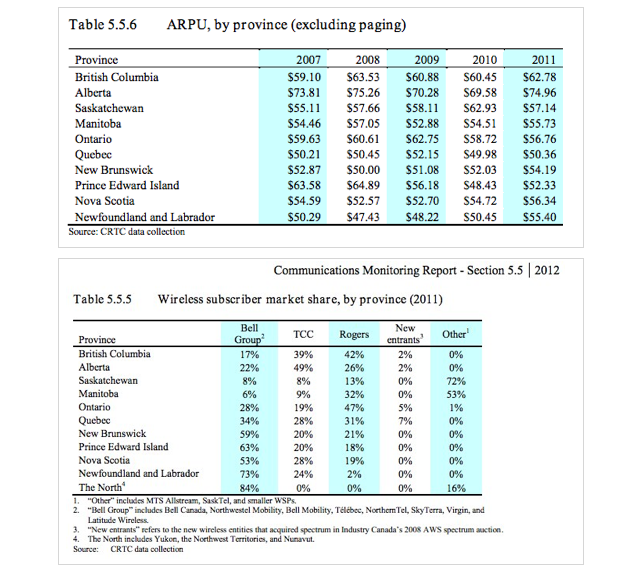

According to the report the number of wireless subscriber in Canada now sits at 27.4 million, up 6% from last year and representing 78.2% of households. As for subscribers, the CRTC says that the new entrants (WIND, Mobilicity, Public Mobile, Videotron) have captured approximately 4% of wireless subscribers and 2% of revenues in 2011.” Take the 4% of 27.4 million and you have 1,096,000. At the end of 2011 WIND Mobile reported their subscriber base reached 403,000 – so this means that the others have a combined total of 693,000. Wireless revenues increased 6.2% from $18.0 billion to $19.1 billion. ARPU (Average revenue per user) also increased in 2011 by 0.2% to $57.98/month.

Other notable stats:

– networks cover approx. 20% of Canada’s geographic area and is available to 99% of Canadians

– LTE network is available to approximately 45% of Canadians

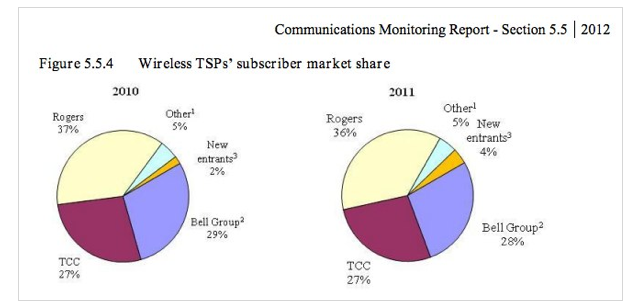

– Rogers had 36% wireless market share, followed by Bell at 28% and TELUS at 27%

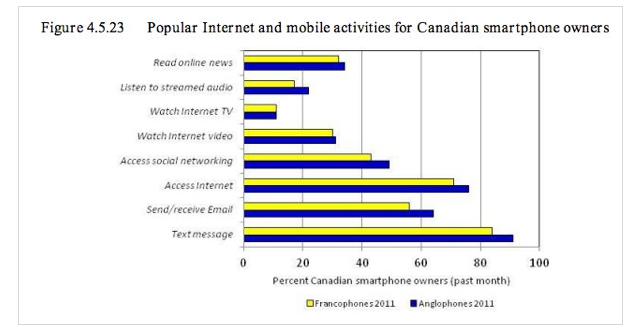

– Texting is still the most popular activity for smartphone owners, followed by accessing the web

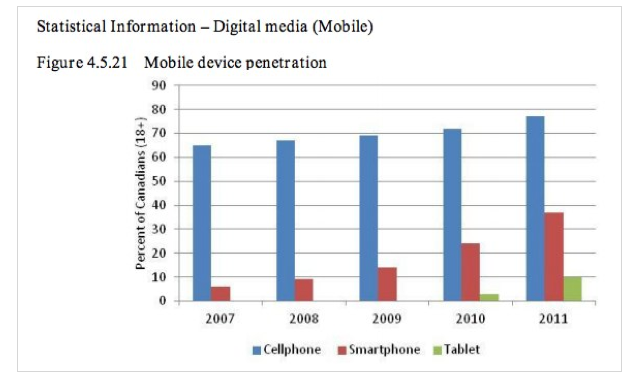

– Tablet usage is around 10%

Developing…

You can check out the full report here at the CRTC

MobileSyrup may earn a commission from purchases made via our links, which helps fund the journalism we provide free on our website. These links do not influence our editorial content. Support us here.